As we look forward to 2025, the global investment landscape is filled with both exciting opportunities and potential challenges. The U.S. economy stands out for its resilience, buoyed by strong consumer spending, technological advancements, and supportive monetary policies. In contrast, China faces a more subdued outlook due to external pressures like U.S. tariffs.

The U.S. economy is expected to grow between 2% and 2.5% in 2025. This growth is driven by:

– Consumer Spending: Americans are continuing to spend, which supports businesses and overall economic health.

– Technological Innovation: Artificial intelligence (AI) is a major growth engine, with spending projected to reach $200 billion by 2025. Both large corporations and small businesses are leveraging AI to boost productivity.

– Robust Labor Market: Although unemployment has risen slightly to 4.2%, job creation remains strong across various industries.

With a Republican administration likely taking office in 2025, we can expect a focus on tax cuts and deregulation. These measures could create a more business-friendly environment, stimulating investment and boosting consumer confidence.

While inflation has moderated to around 2.3%, risks of a resurgence remain due to supply chain issues and strong consumer demand. The Federal Reserve will need to carefully manage monetary policy to balance inflation control with economic growth.

China’s GDP growth is projected to dip below 5% in 2025, primarily due to external pressures like potential tariff increases from the U.S. The Chinese government is responding with increased fiscal support, but significant economic recovery may take time.

China’s property market continues to struggle, with state developers faring better than private ones. A full recovery in property sales and prices is not expected until at least mid-2026.

The fixed income market will face challenges in 2025 as inflation risks could prompt the Federal Reserve to adjust interest rates unexpectedly. Investors should keep an eye on inflation trends, as they will significantly influence bond yields and market conditions.

Gold is likely to perform well in 2025 due to safe-haven demand amid geopolitical uncertainties. In contrast, energy markets may remain subdued despite ongoing tensions in the Middle East.

The U.S. dollar is expected to stay strong thanks to solid economic fundamentals and favourable interest rate differentials compared to other currencies.

Geopolitical tensions, particularly in the Middle East and Ukraine, continue to pose risks but have not significantly affected global financial markets so far. Investors should remain alert to these developments as they could impact market stability.

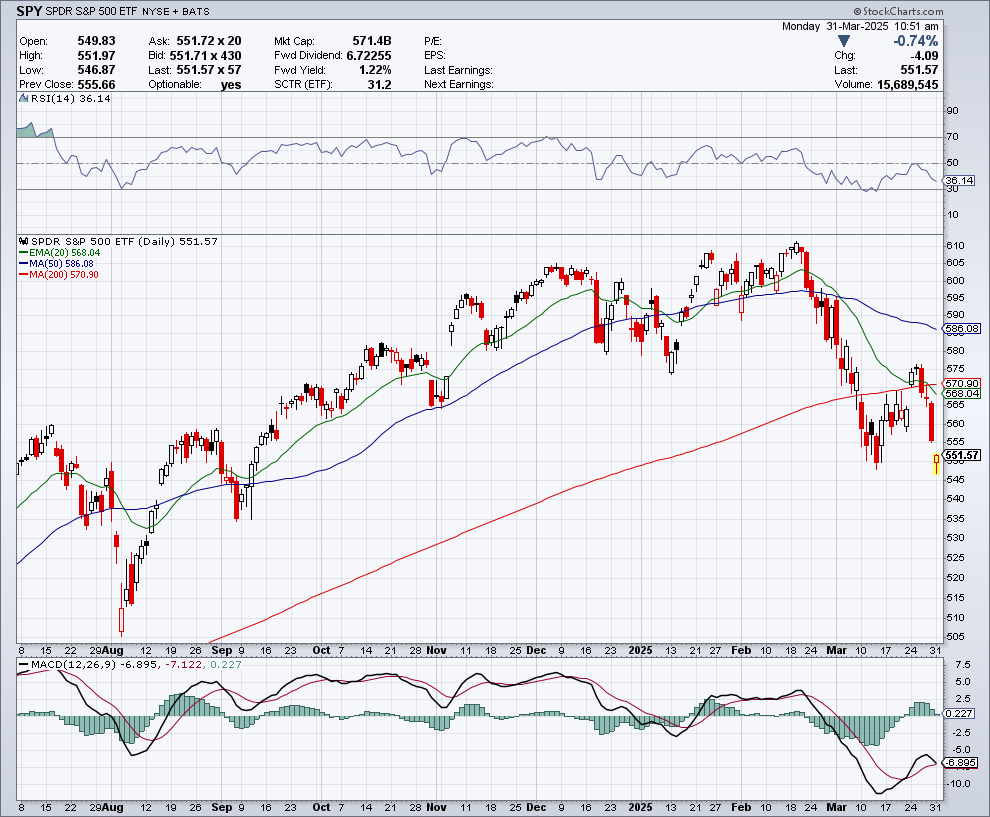

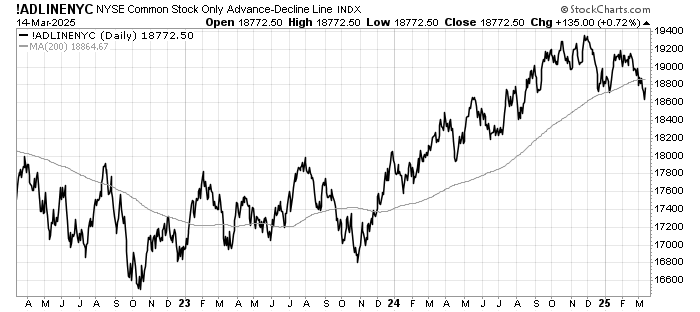

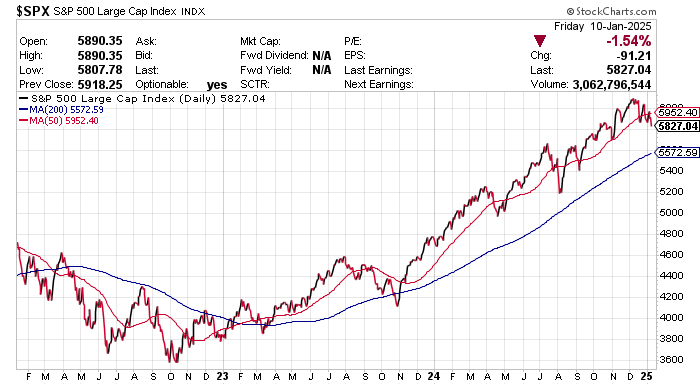

The U.S. stock market appears poised for a strong year ahead, with broad participation across sectors. Despite high valuations, robust earnings growth suggests that the market could continue its upward trend in 2025.

As we head into 2025, the outlook for U.S. equities is generally positive, but it’s important for investors to stay vigilant about potential risks that could disrupt this environment. Monitoring economic indicators, geopolitical developments, and changes in monetary policy will be crucial for making informed investment decisions.