MARKETS IN BRIEF

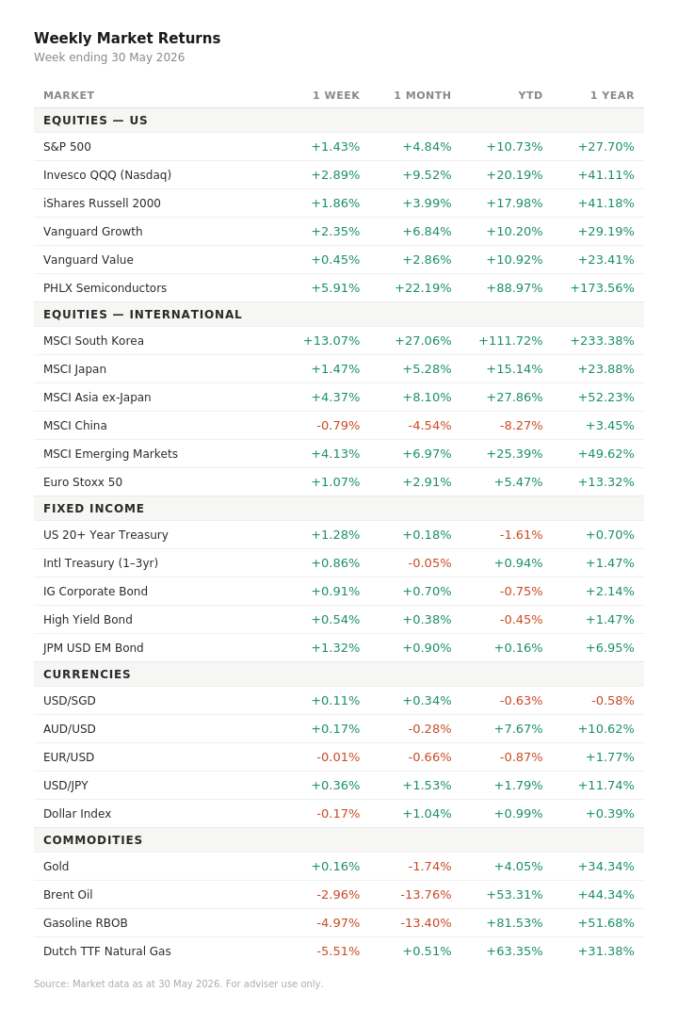

Markets were broadly risk-on this week, with equities rising across most regions and credit spreads tightening, but the mood was driven by a narrow theme rather than broad optimism — the semiconductor and AI hardware trade is doing most of the heavy lifting. The standout move was South Korea, up 13% in a single week, with PHLX semiconductors close behind at nearly 6%; everywhere else, gains were modest. Beneath the surface, the simultaneous rally in both equities and long-duration bonds points to markets pricing in lower rate hike odds.

TOP THEMES THIS WEEK

1. The AI spending boom is hitting a cost ceiling but not stopping. After an initial period of unchecked enthusiasm, companies are beginning to ration their AI usage as costs have escalated far faster than budgets anticipated, with some firms burning through annual AI spending allowances in under three months. This matters because it introduces the first real constraint on the demand side of the AI trade and raises the question of whether the revenue growth that chip and infrastructure companies are pricing in will actually materialise at the pace the market expects.

2. Hyperscaler debt has reached a scale that is reshaping credit markets. Companies like Meta and Alphabet have collectively borrowed over $250 billion to fund AI infrastructure, driving record activity in the credit default swap market as banks seek to offload their concentrated exposure to a handful of mega-borrowers. For investors, this is significant because it means the AI buildout is now a credit market story as much as an equity one.

3. Higher bond yields are here to stay regardless of what happens in the Middle East. Strategists are warning that even a full resolution of the US-Iran conflict and a reopening of the Strait of Hormuz would not bring long-term Treasury yields down materially, because the dominant drivers are now structural: large fiscal deficits, public debt concerns, and a higher long-run neutral rate.

4. US stocks are at dot-com era valuations, but consumers have never been gloomier. The S&P 500 is trading at valuation levels last seen at the peak of the dot-com bubble in 2000, yet US consumer sentiment recently hit its lowest point in 70 years. This disconnect that has no modern precedent. The difference from 2000 is that today’s high valuations rest on AI-driven profit margin expansion rather than shared public euphoria, but the underlying consumer stress, a $1.25 trillion in credit card debt, a 90-day delinquency rate of 13.12%, the highest in 15 years, is a slow-burning risk that equity markets are choosing to ignore.

WATCH THIS NEXT WEEK

South Korea. A 13% weekly gain in a country index is not normal. Korea is up 27% over the past month and 112% for the year — an extraordinary run that makes it the clearest live test of whether the semiconductor rally has genuine fundamental support or whether it has simply run ahead of itself. If this week’s move consolidates, it signals that the market believes the chip cycle has genuinely turned. If it reverses sharply, it will pull semiconductors, QQQ, and the broader AI hardware trade down with it. Either outcome tells us something important about where we are in this cycle.

Leave a Reply