Equity markets ended the week in a broad risk-on mood, with almost every major index posting gains and both large and small caps participating. The dominant force behind the rally remains artificial intelligence hardware — semiconductors were up 6% on the week and have nearly doubled in some Asian markets year-to-date. The one discordant note came from bonds, where long-dated US Treasuries remain under pressure for the year, quietly signalling that not everyone is convinced the good times will last.

The AI hardware trade is not slowing down — it is accelerating. South Korea and Taiwan are the world’s best-performing equity markets this year, powered almost entirely by chipmakers such as Samsung, SK Hynix, and TSMC. This matters because it confirms that the investment cycle is firmly in the physical layer of AI — the chips, the memory, the data centre hardware — rather than in software or platforms.

The Iran war remains the single biggest macro risk — and it is unresolved. The Strait of Hormuz closure has effectively removed around one billion barrels of oil from global supply, and despite President Trump’s suggestion that talks are in their final stages, observers see no sign of either side backing down. Dec 2026 futures prices remain elevated, as markets see a slow recovery in oil supply even as a deal is seen as the most likely outcome.

Interest rates are not coming down — and bond markets are adjusting. The latest US Federal Reserve minutes show a majority of officials are prepared to raise rates further if inflation stays above target, reversing what many had hoped would be a year of cuts. Sovereign bond yields across the G7 are at two-decade highs, and governments are under pressure to fund growing deficits at a much higher cost. This “higher-for-longer” environment is the backdrop against which equity valuations must eventually be judged.

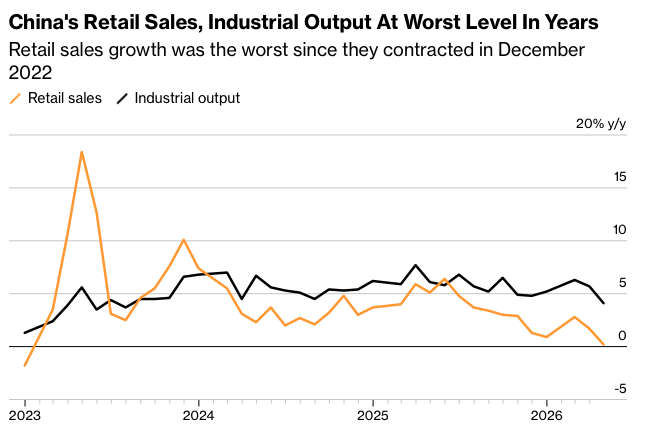

China is the market that the data and the price are both warning about. Domestic spending and investment missed forecasts in April, reflecting an economy where factories and exporters are thriving but ordinary consumers are not. The MSCI China index is the only major equity benchmark in the red for the year (-7.82% YTD), even as Chinese hardware exporters benefit from global AI demand. A few analysts see a mean-reversion opportunity in beaten-down Chinese sectors — but the price action this week does not yet support that view.

Leave a Reply