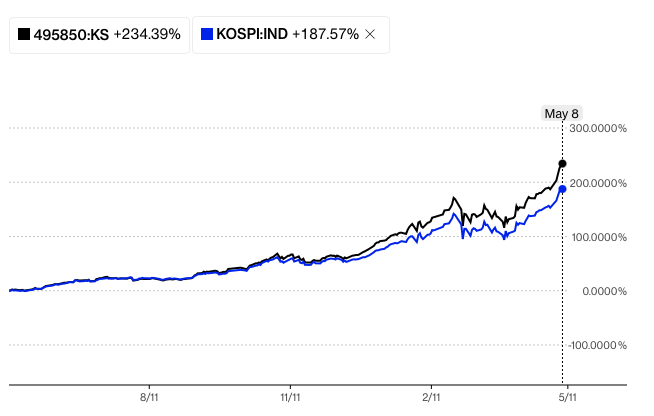

South Korea’s equity market has undergone a historic re-rating in 2026, transforming from a discounted emerging market into the world’s seventh-largest equity market with a market capitalization of US$4.59 trillion. Within five months, it overtook Germany, France, the UK, and Canada. The rally is no longer driven purely by speculation or policy optimism. It is increasingly supported by structural reforms, AI-driven semiconductor earnings, and institutional capital inflows.

The first pillar of the re-rating is governance reform. Historically, the “Korea Discount” reflected weak shareholder protections, opaque chaebol structures, and poor capital allocation. The government’s “Value-Up” reforms and amendments to the Commercial Act have materially changed this framework.

Fiduciary duties now extend to all shareholders, firms face pressure to improve shareholder returns, treasury shares must increasingly be cancelled, and English disclosures have expanded significantly. These measures have improved investor confidence and driven strong outperformance in the Korea Value-Up Index relative to the broader market.

The second pillar is the AI semiconductor boom. South Korea now sits at the centre of the global AI supply chain through its dominance in high-bandwidth memory (HBM) and advanced DRAM production. Samsung Electronics and SK Hynix have become major beneficiaries, with semiconductor firms now accounting for around 45% of the KOSPI. Demand from major cloud companies such as Amazon, Microsoft, Google, and Meta has effectively locked in production capacity for 2026. Exports surged sharply, while Samsung’s operating profit is projected to reach KRW 83 trillion, supported by strong pricing power and supply shortages in memory chips.

The third pillar is the institutionalisation of Korea’s bond market through inclusion in the World Government Bond Index (WGBI). This is expected to attract large foreign inflows, diversify Korea’s investor base, and support the Korean won. However, liquidity issues in long-dated “off-the-run” bonds remain a technical risk.

Despite the bullish outlook, vulnerabilities remain as highlighted by observers. The market is highly concentrated in large-cap technology stocks, retail leverage has risen sharply, and South Korea remains exposed to trade tensions, especially potential US tariff increases. In addition, weaker domestic sectors face refinancing pressures as interest rates rise.

Still, we remain impressed by how other “non-AI” sectors are doing. Financials, consumer discretionary and construction stocks are up double digits this year. There is evidence of broad participation, despite the bubbly-like performance of the Korean tech stocks.

Overall, South Korea is shifting from a market defined by a valuation discount to one increasingly deserving of a structural premium, driven by governance reform, AI earnings power, and deeper institutional integration into global capital markets.

Leave a Reply