17 July 2026

The Big Picture

Banks just reported some of their best profits in history. On the surface, that looks like a strong vote of confidence in the economy and markets. But when one looks closer, the strength is coming from one part of banking — trading and dealmaking — while the more traditional, everyday lending business is turning more cautious. Meanwhile, a separate corner of the credit world (private lending funds) is showing real strain.

So the honest answer is: yes, financials are confirming the bull market, but only part of the sector is doing the confirming, and the part that isn’t is worth watching.

What’s genuinely new: bond yields have jumped because the ceasefire with Iran broke down again on 8 July, pushing oil prices and inflation worries higher. That’s a near-term (under three months) development.

What’s improved: bank profits, driven by trading desks and deal-making. That’s a shorter-term (three to twelve months) trend tied to market volatility, not necessarily something that lasts for years.

What’s deteriorated: private lending funds are under real pressure, with funds restricting investor withdrawals and regulators paying closer attention. That looks like a longer-running (six months to two years) problem, not a passing scare.

What hasn’t changed: everyday credit markets remain calm. Companies can still borrow cheaply, and the Federal Reserve has kept interest rates steady since June, with markets expecting another pause at the end of July.

1. What Bond Yields Are Telling Us

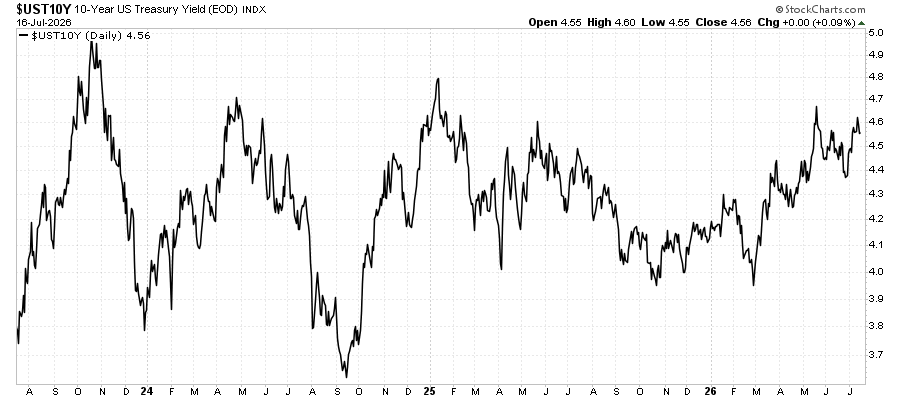

The facts: The 2-year US government bond now yields 4.2%, and the 10-year yields 4.6%. Longer-term yields sit above shorter-term ones, which is the normal, healthy shape for the yield curve. Both yields have risen together since fighting with Iran flared up again on 8 July. The Fed has kept its main interest rate at 3.50–3.75% since June, and futures markets currently expect it to hold rates steady again at its 29 July meeting.

What it means: Short and long-term yields are rising together. This matters because there are two very different reasons yields can climb: either the economy is expected to grow more strongly, or investors are worried about inflation and demanding more compensation for lending money over the long term. Right now, this looks like the second case — an inflation and oil-price story following the renewed conflict, rather than the market suddenly expecting the Fed to cut rates aggressively because of a weakening economy. In fact, futures markets show almost no expectation of near-term rate cuts, which tells us investors are not pricing in a recession.

Why this matters for banks: A more normal-shaped yield curve, where long-term rates sit comfortably above short-term rates, is generally good for bank profitability, because banks borrow short-term (like savings deposits) and lend long-term (like mortgages), earning the difference. Bond markets and share markets currently agree with each other — neither is signalling an imminent downturn.

What could go wrong: If the Iran conflict escalates further and oil prices stay above roughly $80 a barrel, this could turn into a more troubling combination of higher inflation and slower growth. That would be a genuinely negative environment for banks, forcing the Fed to keep rates higher for longer even as the economy weakens.

2. Is Credit Flowing Freely or Drying Up?

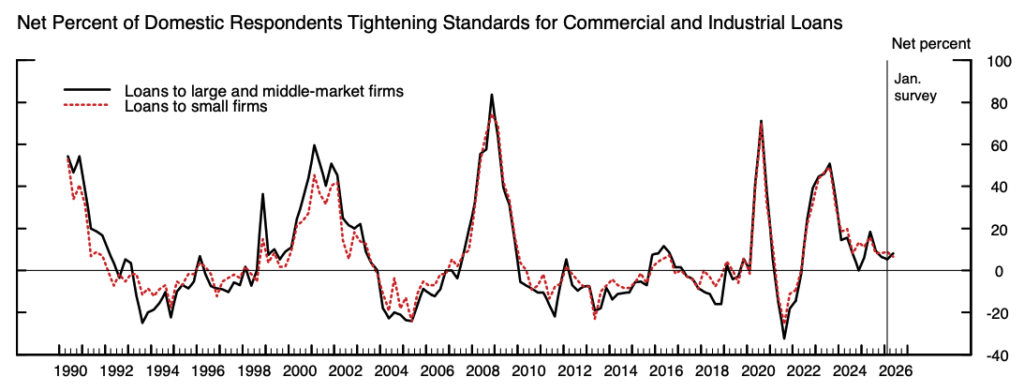

The facts: The Federal Reserve’s latest survey of senior bank loan officers (covering the first quarter of 2026) found that banks are, on balance, tightening their standards for business loans, while demand from borrowers has stayed roughly flat. Banks also said they’ve tightened lending standards over the past year specifically for loans to private lending funds. Separately, a broad measure of financial conditions from the Chicago Fed shows conditions are looser than average overall.

What it means: This is a genuine split. On one hand, banks are becoming more careful about who they lend to directly, especially when lending to other lenders in the private credit space. On the other hand, overall financial conditions remain easy, because companies can still raise money cheaply through the stock and bond markets. In other words, credit is not so much expanding through traditional bank loans right now — it’s flowing more through capital markets and non-bank lenders instead.

Our assessment: Lending standards are tightening at the margin, but conditions overall are not restrictive. This looks like normal late-stage caution from banks, not the start of a credit crunch.

3. Are Credit Markets Still Backing the Rally?

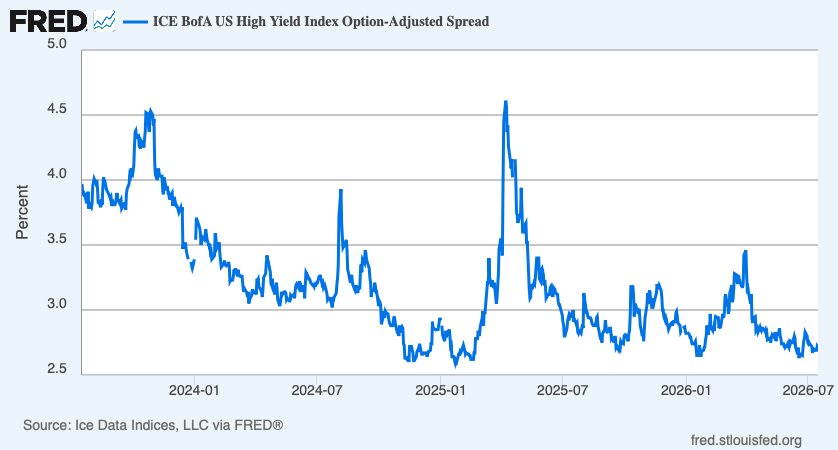

The facts: The extra interest rate that investors demand to lend to riskier, “high-yield” companies (compared with safe government debt) is sitting near its lowest level in years — around 2.4 percentage points.

What it means: When investors demand very little extra compensation to lend to riskier companies, it usually means they see very little risk of default. That’s a vote of confidence, and it’s currently backing up the optimism we’re seeing in share prices. But there’s a catch: spreads this tight leave very little room to move in a positive direction. If sentiment turns, there’s much more room for these gaps to widen (get worse) than to narrow further (get better). So this part of the market is giving investors no early warning of trouble ahead.

The catch to flag: While these public, tradeable credit markets look calm, the private lending market — a roughly $2 trillion industry that is increasingly connected to banks and insurers — is not calm at all (more on this below). So the “all clear” signal from public credit markets may be masking a problem building in a less visible corner of the credit world.

4. How Healthy Is the Financial Sector, Really?

The facts: JPMorgan reported record profits of $21.2 billion for the second quarter — the highest quarterly profit in US banking history — driven by trading activity (up 86% year-on-year in equities) and investment banking fees (up 30%). All five of the largest US banks beat analysts’ expectations this earnings season. Smaller, regional banks have also been outperforming the broader financial sector for much of the year, which is encouraging, because regional banks rely on traditional, everyday lending rather than trading, so their strength is a purer read on the health of the real economy.

What it means: The strongest part of the financial sector right now is the trading and dealmaking side of banking — benefiting from record levels of mergers and acquisitions and heightened market volatility caused partly by the Iran conflict. This is a shorter-term, volatility-driven boost to profits, not necessarily a sign of a structurally stronger banking business built on steady loan growth. Insurance companies, by contrast, have lagged the broader market, partly due to growing concerns about their exposure to private lending funds.

Our assessment: It’s encouraging that both large trading-focused banks and smaller regional lenders are doing well at the same time — that’s a broader, healthier signal than if only one type of bank were leading. But we should be clear-eyed that much of the current profit boost comes from a source (trading revenue) that tends to rise and fall quickly with market conditions, rather than steady, repeatable loan income.

5. Is This Strength Spreading, or Narrowing?

The facts: Smaller US companies (measured by the Russell 2000 index) have returned about 21% so far this year, comfortably ahead of the roughly 10.5% return from the large-company S&P 500 index. A version of the S&P 500 that gives every company equal weight, rather than favouring the very largest firms, has returned about 13%. Even so, the ten largest companies in the S&P 500 still make up around 37–38% of the entire index.

What it means: This is good news. For much of the past couple of years, market gains have been concentrated in a small handful of giant technology companies. Now we’re seeing smaller companies and the “average” stock doing better than the market’s biggest names. That’s the opposite of the narrow, fragile-looking leadership that has often preceded trouble in the past. The strength we’re seeing in financials is being echoed elsewhere in the market, not happening in isolation.

Our assessment: Market participation is broadening, not narrowing. This is a supportive sign, not a warning sign, for how sustainable the current rally is.

6. The Five Biggest Risks to Watch

| Risk | How likely | When it could hit | How big the impact could be | What to watch for early |

|---|---|---|---|---|

| Iran conflict flares up further, oil prices spike | Elevated right now | Next 0–3 months | High — pushes inflation and bond yields higher, keeps the Fed cautious for longer | Oil sustained above $85–90 a barrel; shipping through the Strait of Hormuz slowing |

| Stress in private lending funds spreads to banks and insurers | Moderate | Next 6–18 months | Medium to high — could hit bank and insurer balance sheets directly | More private funds restricting investor withdrawals; insurers writing down private loan values |

| Calm credit markets suddenly turn nervous | Moderate | Next 3–12 months | Medium — a broad repricing of risk across corporate debt | The extra yield demanded on risky company debt rising sharply from today’s low levels |

| Slowdown in AI-related business investment feeds through to markets | Moderate | Next 3–12 months | Medium — this is currently a key driver of the trading and dealmaking profits banks are enjoying | Big technology companies signalling they’ll spend less on AI infrastructure |

| Inflation stays stubbornly high, forcing the Fed to stay tighter for longer even as growth slows | Moderate | Next 6–12 months | High — squeezes bank lending margins and pressures the wider economy | Inflation readings reaccelerating; bond markets pricing in higher long-term inflation even as growth data weakens |

Bottom Line

Is the financial sector still confirming the bull market? Yes, but only part of it. The trading and dealmaking side of large banks, along with regional banks, is confirming strongly. Traditional lending and the private credit corner of the sector are not.

Is this healthy growth, or a warning sign of excess this late in the cycle? A bit of both. Record bank profits and broader participation from smaller companies look genuinely healthy. But credit spreads sitting near record lows, banks quietly tightening lending standards even as profits soar, and real stress building in private lending funds are all classic signs of a market that’s further along in its cycle than the headlines suggest.

What’s the strongest evidence supporting a positive view? Market gains are broadening out to smaller companies and the average stock, rather than being concentrated in a handful of giants. Historically, that kind of broadening has been a healthier, more reassuring signal than narrow leadership.

What’s the strongest evidence against it? The gap between glowing trading profits and quietly tightening bank lending standards, combined with a private lending market genuinely under stress for the first time since it grew large, suggests the sector’s headline strength is concentrated in the part of the business most exposed to a sudden swing in market mood, not the part that reflects steady, everyday demand for credit in the economy.

What would change our view? Three things would move us from “cautiously positive” to genuinely worried: a sharp and sustained rise in the extra yield demanded on risky corporate debt; another quarterly bank survey showing broad, deepening reluctance to lend alongside weakening demand; or clear evidence that stress in private lending funds is spreading onto the balance sheets of mainstream banks.

Leave a Reply